![]() Call us now:

Call us now:

If you are dealing with an insurance claim, vehicle valuation dispute, estate matter, or financial review, you will almost certainly encounter the terms fair market value and actual cash value (ACV). While they are often used interchangeably, they are not the same, and misunderstanding the difference can materially affect the outcome of a claim, settlement, or financial decision.

As a certified auto appraiser and licensed adjuster, I see this confusion regularly. In many cases, vehicle owners, attorneys, and financial institutions rely on valuation terminology that sounds authoritative but does not reflect the correct valuation standard for the situation. Understanding how fair market value and ACV differ and when each applies is critical.

This article explains those differences, how each value is determined, and when an independent appraisal may be necessary.

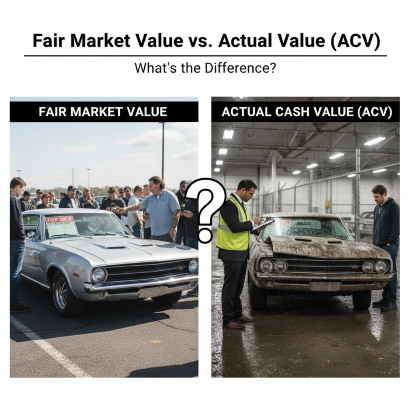

What Is Fair Market Value?

Fair market value refers to the price a vehicle would sell for in an open and competitive market between a willing buyer and a willing seller, with neither under compulsion and both having reasonable knowledge of the relevant facts.

This definition aligns with how fair market value is applied in legal, estate, and financial contexts. The IRS uses a similar standard when determining fair market value for tax and estate purposes, defining it as the price at which property would change hands under normal market conditions

(Source: IRS Fair Market Value definition, https://www.irs.gov).

In real-world vehicle appraisals, fair market value is influenced by:

- Current supply and demand

- Geographic market conditions

- Vehicle condition and mileage

- Comparable vehicle sales

- Equipment, options, and configuration

Fair market value is commonly used in estate and probate appraisals, private party sales, legal disputes, and financial reporting where a realistic market based value is required.

When I prepare a fair market value appraisal, the objective is to reflect what the vehicle would reasonably sell for, not a formula generated number detached from market realities.

What Is Actual Cash Value (ACV)?

Actual cash value (ACV) is most often used in insurance related matters, particularly total loss claims. ACV is typically defined as the replacement cost of a vehicle minus depreciation, based on its condition immediately prior to the loss.

In practice, ACV determinations are usually generated using third party valuation systems and may rely on:

- Algorithm based depreciation models

- Limited or poorly matched comparable vehicles

- Preset adjustment limits

- Automated condition assumptions

This approach can create problems when the valuation does not accurately reflect the vehicle’s true pre loss condition or the local market.

I regularly review ACV reports that appear precise but rely on inappropriate comparables or unsupported deductions, which often leads to undervalued settlement offers.

Fair Market Value vs. Actual Cash Value: Key Differences

Understanding the distinction between fair market value and ACV requires looking at purpose, methodology, and flexibility.

Purpose and Use Case

- Fair market value is used to determine what a vehicle would realistically sell for

- ACV is used to determine what an insurer believes it owes under a policy

Using the wrong valuation standard can lead to disputes, delays, or financial loss.

Valuation Methodology

Fair market value relies heavily on real world market data and comparable sales. ACV often relies on formula driven calculations with limited discretion.

While ACV is not inherently incorrect, it should be carefully reviewed for accuracy.

Professional Judgment and Flexibility

Fair market value appraisals allow for professional judgment when accounting for:

- Condition differences

- Regional demand

- Vehicle rarity or configuration

- Modifications or specialty use

ACV calculations often restrict those adjustments, which is a frequent source of disagreement.

Why the Difference Matters in Total Loss Insurance Claims

In total loss situations, insurers typically base settlement offers on ACV. However, if the ACV calculation is flawed or unsupported, the resulting offer may not reflect the vehicle’s true pre-loss value.

This is where independent appraisal support becomes important.

When reviewing ACV determinations, I evaluate:

- Comparable vehicle selection

- Mileage and condition adjustments

- Geographic relevance

- Equipment accuracy

- Unsupported depreciation

If the ACV is not defensible, it can often be challenged.

👉 Related service:

https://www.auto-praise.com/total-loss-appraisals/

Fair Market Value and ACV in Financial and Lending Decisions

Fair market value and ACV are also used by banks, credit unions, and financial institutions when evaluating loan collateral and managing risk.

In these cases, accuracy is critical. An overstated value increases exposure. An understated value can restrict lending or create disputes later.

Independent appraisals provide institutions with transparent, defensible valuations rather than relying solely on automated systems.

👉 Related article:

https://www.auto-praise.com/acv-appraisals-financing/

When an Independent Vehicle Appraisal Is Needed

You should strongly consider an independent appraisal when:

- A total loss offer appears undervalued

- Comparables do not match your vehicle’s condition

- A valuation is required for estate, legal, or financial purposes

- A lender requires defensible documentation

- There is a dispute over valuation methodology

An independent appraisal provides a neutral, third party assessment supported by data and professional judgment.

👉 https://www.auto-praise.com/fair-market-valuation/

Fair Market Value vs. Actual Cash Value: Which Applies to Your Situation?

The correct valuation depends on why the value is needed, not just the terminology being used.

- Insurance total loss claims: ACV (but it must be accurate)

- Estate or probate matters: Fair market value

- Loan collateral evaluations: ACV or fair market value depending on policy

- Private-party transactions: Fair market value

Understanding this distinction helps you evaluate offers, challenge inaccuracies, and make informed decisions.

Final Thoughts

Fair market value and actual cash value serve different purposes and are calculated differently. Confusing the two or relying on an unsupported valuation can put you at a disadvantage.

Whether you are dealing with an insurance claim, financial institution, or legal matter, knowing which valuation standard applies is essential.

Related Links

Can an insurance company use fair market value instead of ACV for a total loss?

In most insurance policies, total loss settlements are based on actual cash value (ACV), not fair market value. However, the ACV still must be calculated accurately and reflect the vehicle’s true pre loss condition and market context. When the ACV calculation is flawed or unsupported, it can often be challenged using an independent appraisal.

Do vehicle modifications increase fair market value but not ACV?

Often, yes. Certain modifications, restorations, or specialty equipment may positively influence fair market value, especially in private party or collector markets. Insurance ACV calculations frequently limit or exclude credit for modifications unless they are specifically endorsed on the policy. This disconnect is a common source of valuation disputes.

How does vehicle condition documentation affect ACV calculations?

Condition documentation can significantly impact ACV. Photos, service records, inspection reports, and repair invoices help establish the vehicle’s true pre loss condition. Without proper documentation, insurers may apply generic condition assumptions that do not reflect reality.

Are online car value tools reliable for determining ACV or fair market value?

Online valuation tools can provide a general reference point, but they are not appraisals. They often rely on broad data sets and automated assumptions that fail to account for condition, configuration, or local market factors. For insurance, legal, or financial matters, a professional appraisal is typically far more defensible.

When do banks or lenders require an independent ACV appraisal?

Financial institutions may require an independent ACV appraisal when collateral value affects underwriting decisions, loan restructuring, dispute resolution, or risk exposure. In these situations, lenders often need documented, third-party valuation support rather than automated valuation outputs alone.