![]() Call us now:

Call us now:

A 2017 Honda Civic Hatchback Sport Touring, garaged in Weston, Florida, was declared a total loss following a March 2026 accident. The vehicle’s insurer opened with a base vehicle value of $9,831 — a figure built on comparables pulled from as far away as Tampa and Bartow, two of which weren’t even the correct model year. An independent appraisal from Auto Praise, following in-person inspection of the vehicle, valued it at $16,718.27. After the vehicle owner invoked the appraisal clause, the two appraisers reached a binding agreement of $15,000 — $5,169 above the insurer’s initial base value, without the case requiring umpire involvement.

Case Overview Table

| Vehicle | 2017 Honda Civic Hatchback Sport Touring |

| Exterior Color | White |

| Engine / Drivetrain | 1.5L turbocharged 4-cylinder, CVT, front-wheel drive |

| Mileage at Time of Loss | 135,031 |

| Location | Weston, FL (Broward County) |

| Service Type | First-party total loss appraisal / appraisal clause |

| Insurer’s Base Vehicle Value | $9,831 |

| Auto Praise Independent Appraisal Value | $16,718.27 |

| Final Appraisal Award | $15,000 |

| Recovery Above Insurer’s Base Offer | $5,169 |

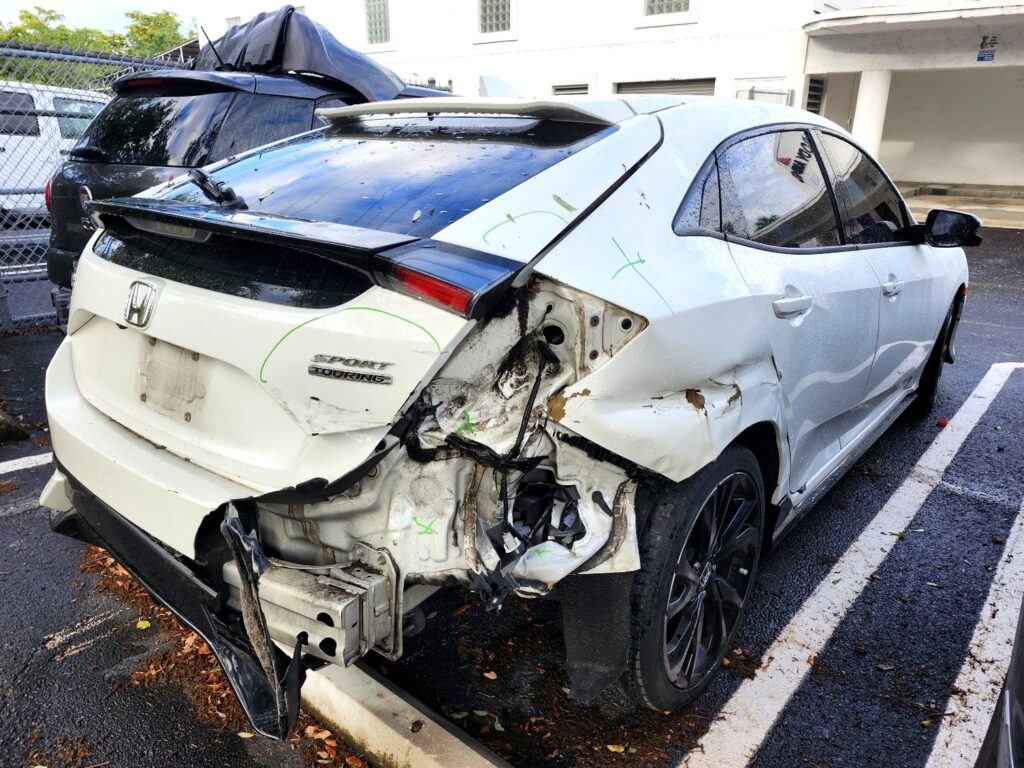

2017 Honda Civic Sport Touring with severe rear-end collision damage photographed in Weston Florida for total loss appraisal

Florida Total Loss Appraisal & Claim Support

- Professional Authority: I-CAR Platinum & IACP Certified Appraisers with Florida 6-20 Adjuster Licensing.

- Industry Credentials: Over 30 years of specialized automotive and insurance claims experience.

- Valuation Experts: Independent Actual Cash Value (ACV) reports designed to accurately value your vehicle.

- Proven Reputation: Five-Star Rated Florida independent appraisal firm providing statewide remote and mobile support.

A Weston Vehicle the Valuation Software Placed in Fort Lauderdale

The vehicle owner in this case lives off Sandpiper Circle, inside one of Weston’s residential communities near Bonaventure Boulevard and Royal Palm Boulevard, a short drive from Weston Town Center and the Sawgrass Expressway (SR 869) corridor that connects Weston to the rest of Broward County. Weston sits between the Everglades to the west and the I-75 corridor to the east, and its ZIP code, 33327, is one of the more recognizable residential codes in the county, home to master-planned neighborhoods, top-rated schools, and Cleveland Clinic Weston’s main campus off Cleveland Clinic Boulevard.

That’s part of what makes one detail in this file notable: the insurer’s own valuation report listed the loss vehicle’s location as “Fort Lauderdale, FL 33327,” despite 33327 being a Weston ZIP code, not a Fort Lauderdale one. It’s a small labeling detail, but it matters, because the ZIP code is the starting point the insurer’s automated valuation software uses to search for comparable vehicles. A mislabeled city doesn’t necessarily change which comparables get pulled, but it’s worth flagging when reviewing a market valuation report line by line, which is exactly the kind of detail an independent vehicle appraisal is built to catch.

The Weston used-car market skews toward well-maintained, single-owner vehicles, a reflection of the city’s demographics and its distance from the higher-turnover rental and fleet markets closer to the airport and coastal Fort Lauderdale. A high-mileage but well-documented Civic Sport Touring, like this one, competes in a market where service history and condition carry real weight.

The Insurer’s Valuation — What the Market Report Showed

The insurer’s automated valuation software returned a base vehicle value of $9,831, later reduced by a $235 condition adjustment for driver’s seat wear, bringing the adjusted vehicle value to $9,596. After applicable tax, title, and registration fees were added and the policy deductible subtracted, the insurer’s total settlement figure came to $9,801.11.

That base value was built from five comparable vehicles: three primary comps and two additional listings. Mileage on the vehicle was reported accurately at 135,031 — that part of the file checked out. The comparable selection, though, raised a few questions:

- Two of the five comparables were the wrong model year. The additional comparables pulled from Naples and Sarasota were both 2018 Honda Civics, not 2017s, a detail that matters for trim-year equivalency even within the same generation.

- The search radius extended well outside Broward County. Comparables were sourced from Fort Lauderdale, Bartow (150 miles away), and Tampa (183 miles away). Expanding the search radius when local, matching-mileage inventory is limited is standard appraisal practice, and the insurer applied market adjustments to account for it, but it’s still worth noting how far the net was cast for a vehicle garaged in one of Broward’s most populated western suburbs.

- Several condition categories were marked “no photos” or “photos do not support.” The engine, transmission, tires, carpets, and headliner were all left at a default private-owner condition rating because the underlying documentation didn’t support a more specific finding. Only the driver’s seat received a downward adjustment, based on visible wear.

None of this means the insurer’s tool was operating in bad faith, automated valuation platforms are a legitimate starting point for a total loss estimate. The question in every case is whether the specific comparables and condition inputs accurately reflect the vehicle actually being valued, and in this file, several of them didn’t quite line up.

The Auto Praise Independent Appraisal — Our Process

I personally inspected this vehicle in person, documenting the VIN plate, odometer reading, interior wear, and exterior condition panel by panel. That inspection confirmed the mileage reported in the insurer’s file and gave me a direct look at the driver’s seat wear the insurer had already flagged, which I factored into my own adjustment rather than disputing it.

Where my comparable selection diverged from the insurer’s was in trim and history matching. I limited my search to genuine Sport Touring trim vehicles with the correct 1.5L turbocharged CVT drivetrain, no substituting a different trim level or model year to fill out a comp set. That search turned up very few local vehicles in the same mileage range without accident history, so like the insurer, I expanded the search outward and adjusted for what I found: two of my three comparables carried prior accidents on their vehicle history reports, and I applied history adjustments of $1,499 and $1,700 respectively to bring them in line with the subject vehicle’s clean record. The third, an accident-free comparable, needed no such adjustment.

After mileage and condition adjustments, my three comparables landed at $17,431.95, $17,649.15, and $15,073.70 — an average of $16,718.27, which became my final Actual Cash Value conclusion as of the March 2026 date of loss, certified under USPAP.

I also cross-referenced a Black Book clean retail value of $18,975 for the same vehicle as of the loss date, which supported the direction of my comp-based conclusion even though I didn’t rely on it as the primary methodology.

The Appraisal Clause Process

This was a first-party claim, the vehicle owner was filing under his own policy, which is a requirement for invoking the appraisal clause in the first place. The appraisal clause is only available to a first-party insured; on a third-party claim, where a different driver caused the damage and the vehicle owner is filing against the at-fault driver’s insurance, this process isn’t available, and claimants have to pursue other avenues to challenge a low offer.

After receiving the insurer’s initial valuation, the vehicle owner invoked the clause in writing and named Auto Praise as his appointed appraiser. The insurer appointed its own appraiser. As is standard under Florida policy language, both sides also had the option to name an umpire if the two appraisers couldn’t agree — but that step wasn’t needed here. The two appraisers exchanged their respective market data and reached a binding agreement directly.

Final Agreed Actual Cash Value: $15,000

That figure is the amount the insurer is contractually required to settle the claim for, excluding deductible, tax, and title fees, which are handled separately.

Outcome Summary

| Insurer’s Initial Base Value | $9,831 |

| Final Appraisal Award | $15,000 |

| Recovery | $5,169 above the insurer’s initial base value |

For this vehicle owner, that recovery represented the difference between a settlement that undervalued a well-documented, single-owner Civic and one that reflected what the vehicle was actually worth in the Weston-area market.

What This Case Illustrates

Model-year matching isn’t optional. Two of the insurer’s five comparables were 2018 Civics rather than 2017s. In a generation that carries mid-cycle updates, even a one-year gap can affect equipment, warranty status, and buyer perception, all of which show up in resale price.

A wide search radius isn’t automatically a problem — but it deserves a second look. Comparables from Tampa and Bartow aren’t disqualifying on their own; expanding outward is normal when local mileage-matched inventory runs thin. What matters is whether the adjustments applied to those out-of-area comps actually account for the differences between markets.

“No photos” isn’t the same as “good condition.” Several mechanical and interior categories in the insurer’s file defaulted to a private-owner condition rating simply because supporting photos weren’t available — not because anyone confirmed that condition in person.

Accident-history adjustments cut both ways. Comparable vehicles with a prior accident on record needed upward adjustments to fairly compare against this vehicle’s clean history, a step that’s easy to skip if the comp search isn’t reviewed line by line.

A single ZIP code can carry two different labels in two different systems. Whether or not it changed the outcome here, a Weston address showing up as “Fort Lauderdale” in a valuation report is a reminder to check the basic geographic inputs before trusting the output built on top of them.

Frequently Asked Questions

Why did the insurer’s estimate come in so much lower than the independent appraisal?

The gap largely came down to comparable vehicle selection. The insurer’s file included two comparables that were the wrong model year, and several vehicle condition categories defaulted to a baseline rating because supporting photos weren’t available. Auto Praise’s independent appraisal limited its comparable search to matching trim, model year, and drivetrain, and applied accident-history adjustments where comparables didn’t share the subject vehicle’s clean record. Smaller differences in methodology like these can add up to a meaningful gap in the final number.

What is the appraisal clause, and can any Weston vehicle owner use it?

The appraisal clause is a provision in most Florida auto policies that lets a policyholder demand an independent, binding valuation when they disagree with the insurer’s total loss offer. It’s only available to first-party insureds, someone filing a claim under their own policy. If the claim is against another driver’s insurance instead, this process isn’t available, and other options have to be pursued to challenge the offer. Weston vehicle owners with a first-party total loss claim can generally invoke it by notifying their insurer in writing and naming an appraiser. Learn more in our full Florida Total Loss Claim Guide.

Does the mileage on my car matter more than its condition?

Both matter, but they’re evaluated differently. Mileage is a fairly objective, verifiable number, it either matches the odometer or it doesn’t. Condition is more subjective and depends heavily on documentation: photos, service records, and physical inspection. In this case, the insurer’s mileage figure was accurate, but several condition categories were left undetermined for lack of supporting photos, which is part of why an independent review can turn up a different number even when the mileage inputs agree.

How does an appraiser account for a comparable vehicle that had a prior accident?

When a comparable vehicle has a documented accident on its history report and the loss vehicle doesn’t, the appraiser applies an upward adjustment to that comparable to make it a fair stand-in for a clean-history vehicle. In this case, two of the three primary comparables carried prior accidents, and adjustments of roughly $1,499 and $1,700 were applied to account for that difference before those figures were averaged into the final value.

What should a Weston vehicle owner do if their total loss offer seems low?

Start by requesting a copy of the insurer’s full market valuation report, not just the summary page. Look at where the comparable vehicles came from, what trim and model year they actually are, and whether any condition ratings were left at a default because documentation was missing. If the offer still seems low after that review, Auto Praise offers a free claim review to help determine whether there’s a basis to challenge it and pursue a better settlement.

Was Your Weston Total Loss Offer Accurate?

Every total loss file has its own quirks, the wrong model year in a comp set, a ZIP code that doesn’t match the actual city, a condition rating with no photo behind it. None of these are necessarily signs of bad faith, but they’re exactly the kind of detail that’s easy to miss without a line-by-line review.

If you’re a Weston vehicle owner and your insurance company’s total loss offer seems too low, Auto Praise can review the market valuation report and identify errors that may be affecting your settlement amount. We assist Florida vehicle owners statewide by reviewing comparable vehicles, adjustments, options, condition ratings, and valuation methodology to determine whether the offer is accurate.

A free claim review can help you understand whether there is a valid basis to challenge the insurance company’s valuation and pursue a better settlement.

Call 754-210-9807 for a Free Review Florida Licensed Adjusters • I-CAR Platinum Certified • IACP Certified Auto Appraisers