![]() Call us now:

Call us now:

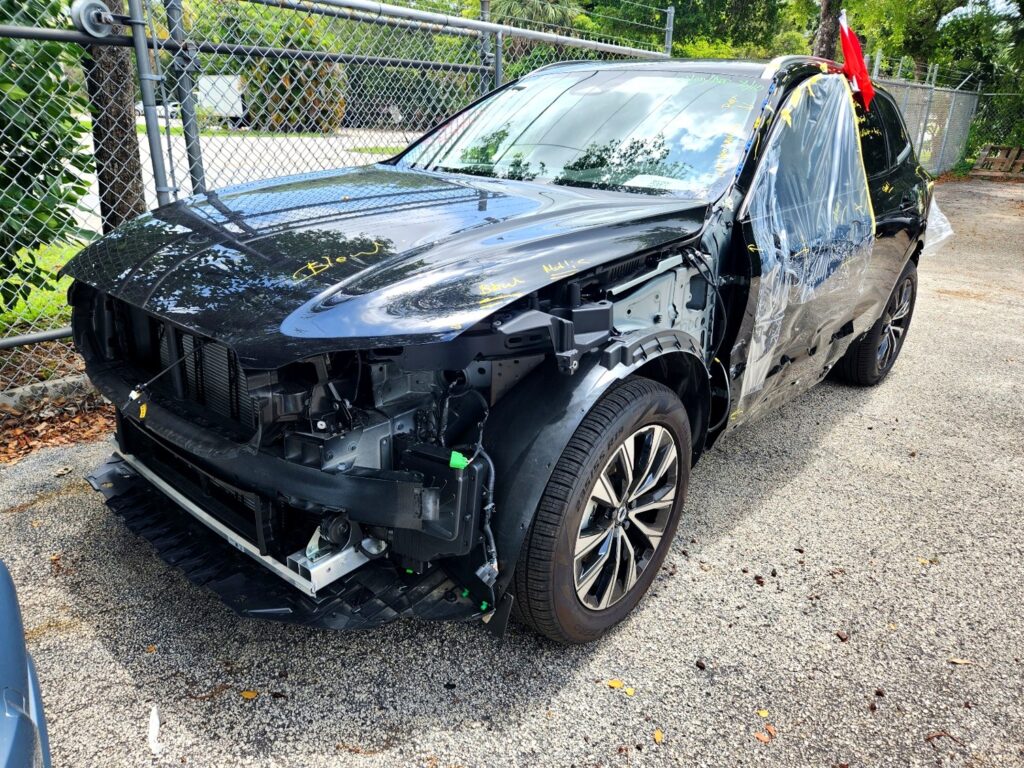

A 2025 Volvo XC90 T8 Ultra Plug-In Hybrid, finished in black, was declared a total loss after an accident in North Broward County near Pompano Beach. The insurer’s market valuation report placed the vehicle’s adjusted value at $55,282. Auto Praise’s independent appraisal concluded a fair market value of $65,313.97. After the vehicle owner invoked the appraisal clause, the two appraisers reached a signed agreement at $63,500 — $8,218 above the insurer’s adjusted valuation.

This case turned on trim equivalency. The insurer’s own primary comparables were a lower “Plus” trim rather than the subject vehicle’s “Ultra” trim, and passenger-configuration differences complicated the comparison further. Here is how the numbers broke down, and what the file shows about how each figure was reached.

Case Overview Table

| Detail | Figure |

| Vehicle | 2025 Volvo XC90 T8 Ultra Plug-In Hybrid |

| Exterior color | Black |

| Engine / Drivetrain | 2.0L I4 turbocharged plug-in hybrid, automatic transmission, all-wheel drive |

| Mileage at time of loss | 17,283 miles |

| Location | Pompano Beach / North Broward County, FL |

| Service type | Independent total loss appraisal, appraisal clause invocation |

| Insurer’s base vehicle value | $51,747.00 |

| Insurer’s condition-adjusted value | $55,282.00 |

| Auto Praise independent appraisal value | $65,313.97 |

| Final signed appraisal award | $63,500.00 |

| Recovery above insurer’s adjusted value | $8,218.00 |

2025 Volvo XC90 with severe front-end and passenger side collision damage in Pompano Beach assessed for total loss appraisal.

Florida Total Loss Appraisal & Claim Support

- Professional Authority: I-CAR Platinum & IACP Certified Appraisers with Florida 6-20 Adjuster Licensing.

- Industry Credentials: Over 30 years of specialized automotive and insurance claims experience.

- Valuation Experts: Independent Actual Cash Value (ACV) reports designed to accurately value your vehicle.

- Proven Reputation: Five-Star Rated Florida independent appraisal firm providing statewide remote and mobile support.

Pompano Beach and the North Broward Vehicle Market

Case records place this loss in the North Broward corridor near Pompano Beach, close to the Deerfield Beach line. This stretch of Broward County sits between two distinct commercial zones: the US-1/Federal Highway retail strip that runs through central Pompano Beach, and the newer commercial development along Powerline Road and Copans Road closer to the Sample Road interchange with I-95.

Vehicle owners in this corridor commonly cross into neighboring Coconut Creek, Parkland, and Deerfield Beach for dealership service and sales, which is part of why an independent total loss appraisal benefits from pulling comparable vehicles across the wider North Broward and South Palm Beach market rather than a single ZIP code.

The market for late-model luxury SUVs in this area is active and closely watched. A 2025 Volvo XC90 T8 Ultra with plug-in hybrid drivetrain is a specialty configuration, buyers in this segment pay close attention to trim level, passenger configuration, and options, which is exactly where this valuation dispute originated.

The Insurer’s Valuation — What the MVR Showed

The insurer’s market valuation report used the insurance company’s automated valuation software to search a national vehicle database and select comparable vehicles. The report generated a base vehicle value of $51,747.00, then applied a condition adjustment of $3,535.00 — largely tied to interior wear and soiling consistent with a vehicle handled and transported through storage yards after a loss, bringing the adjusted value to $55,282.00.

Three primary comparable vehicles were used in the calculation. Two of the three were listed as the “T8 Plus” trim, one step below the subject vehicle’s “T8 Ultra” trim. Only one comparable matched the Ultra trim exactly, and that vehicle carried a different passenger configuration and disclosed prior accident history, which triggered a $6,200 downward adjustment on that comparable alone.

Two of the three comparables were also configured with 7-passenger seating rather than the subject vehicle’s 6-passenger layout, a distinction that traces back to the VIN’s build code rather than a simple option choice. The report did apply upward trim and equipment adjustments to account for some of these differences, and mileage adjustments were made on all three comparables, each of which had meaningfully lower mileage than the subject vehicle’s 17,283 miles at loss.

This isn’t a case of the insurer using improper data, automated valuation software is a legitimate and standard starting point for total loss claims, and the geographic search radius used here was reasonable for a specialty plug-in hybrid SUV. The question is simply whether “Plus” trim comparables, even after adjustment, produce a defensible value for an “Ultra” trim vehicle, and whether the passenger-configuration and mileage adjustments applied were sized correctly for this specific vehicle.

The Auto Praise Independent Appraisal — Our Process

This appraisal was completed as a documentation and photo-based desk review, consistent with how most Auto Praise total loss files are handled, a physical inspection was not required to reach a defensible conclusion in this case.

I reviewed the insurer’s market valuation report, the vehicle’s equipment list, and the photos provided, then built an independent comparable set using a search radius extending beyond South Florida to confirm accuracy. Within a 500-plus mile radius, only one listing matched the subject VIN’s exact build, everything else required careful trim and configuration comparison rather than a straight VIN match.

The subject vehicle’s VIN build code identifies it as a 6-passenger configuration. I cross-referenced this against Black Book data, which shows only a roughly $500 MSRP difference between the 6-passenger and 7-passenger configurations on this platform — a materially smaller gap than the insurer’s comparable set implied when two of three primary comparables carried the 7-passenger layout. I selected three comparables that matched the Ultra trim level and 2.0L plug-in hybrid drivetrain, then applied condition, equipment, mileage, and accident-history adjustments to each individually rather than relying on a single averaged trim adjustment.

The comparable with disclosed prior accident history received a downward adjustment reflecting that history, consistent with how a knowledgeable buyer would price that vehicle against a clean-history subject vehicle. After adjustments, the average comparable value across the three vehicles came to $65,313.97, which also aligned closely with the Black Book Price Point retail value of $63,750 for the same vehicle, mileage, and market. That average became the final Auto Praise value conclusion as of the date of loss.

The Appraisal Clause Process

Because this was a first-party claim filed through the vehicle owner’s own insurer, the vehicle owner had the right to invoke the appraisal clause found in most Florida auto policies. It’s worth noting that the appraisal clause is only available to a first-party insured, meaning the vehicle owner is filing through their own policy. On a third-party claim, where a different driver’s insurer is handling the loss, the appraisal clause is not available, and claimants must pursue other means to challenge an unsatisfactory offer.

In this case, the vehicle owner formally invoked the clause and appointed Auto Praise as their independent appraiser. The carrier appointed its own appraiser in response. As is standard practice under Florida policy language and statute, an umpire was designated at the outset of the process in case the two appraisers could not agree, but that step was not needed here. The two appraisers reviewed their respective valuations and reached a mutual agreement without requiring umpire involvement.

The result was a signed appraisal award establishing the vehicle’s Actual Cash Value at $63,500.00. Under Florida law and standard policy language, this figure is binding, once both appraisers sign the award, the insurance carrier is required to settle the total loss claim based on that amount.

Outcome Summary

Insurer’s Adjusted Valuation: $55,282.00

Final Signed Appraisal Award: $63,500.00

Recovery: +$8,218.00

The $8,218 difference represents real dollars returned to the vehicle owner that would otherwise have been left on the table based on the insurer’s initial trim and configuration assumptions. This outcome reflects the facts of this specific claim file and is not a guarantee of any particular result in a different case.

What This Case Illustrates

Trim equivalency is not optional. A “Plus” trim comparable is not a substitute for an “Ultra” trim vehicle, even with dollar adjustments applied. When two of three primary comparables in a valuation come from a lower trim tier, the resulting average value carries that gap forward unless the adjustments are sized to fully close it.

VIN build codes decide passenger configuration, not assumptions. The difference between 6-passenger and 7-passenger seating on this platform carries only a modest MSRP difference, but it still shapes which vehicles qualify as true comparables. Reading the VIN’s build digit directly settles the question rather than guessing from photos or listings.

Desk reviews can be just as defensible as physical inspections. Most total loss appraisals, including this one, are completed using documentation, photos, and market data rather than an in-person inspection. What matters is the quality of the comparable selection and adjustment methodology, not whether an appraiser stood next to the vehicle.

Condition adjustments should reflect actual wear, not assumptions from limited photos. Both the insurer and Auto Praise noted limits on what could be determined from available photos alone. Careful, itemized condition review, component by component, produces a more defensible number than a single blanket adjustment.

The appraisal clause exists precisely for disputes like this one. When a first-party policyholder and their insurer can’t agree on value, Florida policy language provides a structured path to resolve it — one that, in the large majority of cases including this one, resolves through direct agreement between the two appointed appraisers rather than requiring an umpire.

Frequently Asked Questions

What is a Market Valuation Report (MVR), and why did the insurer’s number differ from Auto Praise’s number?

An MVR is the report an insurance company generates using automated valuation software to estimate a total loss vehicle’s value. It searches a vehicle database, selects comparable vehicles, and applies adjustments for mileage, condition, and equipment. In this case, the insurer’s comparable set leaned on a lower trim level than the subject vehicle, which pulled the resulting value down. Auto Praise’s independent review selected comparables matching the exact trim and applied adjustments individually rather than relying on the insurer’s averaged approach, producing a higher supported value.

Does a total loss appraisal always require a physical inspection of the vehicle?

No. Most Auto Praise total loss appraisals, including this one, are completed as desk reviews using photos, vehicle history, equipment data, and market comparables. A physical inspection can add value in specific situations, but it is not the standard requirement for a defensible independent appraisal, and its absence does not weaken a properly documented conclusion.

Can I invoke the appraisal clause on any total loss claim in Florida?

The appraisal clause is available only to a first-party insured, someone filing a total loss claim through their own auto policy. If a different driver caused the accident and you are filing against that driver’s insurance company as a third-party claimant, the appraisal clause is not available to you, and you would need to pursue other avenues to challenge a low offer, such as direct negotiation or legal counsel.

What happens if the two appraisers in an appraisal clause dispute can’t agree?

Florida policies typically require an umpire to be selected at the start of the appraisal process as a safeguard, in case the two appointed appraisers reach an impasse. In practice, the large majority of appraisal clause cases, including this one, resolve through direct agreement between the two appraisers, and the umpire is never actually needed to decide the value.

My total loss offer in Pompano Beach seems low — what should I do first?

Start by requesting a copy of the insurer’s full market valuation report, not just the settlement letter. Review the trim level, mileage, and passenger or equipment configuration of every comparable vehicle listed against your actual vehicle’s specifications. If the offer seems low once you compare those details, an independent appraisal can identify whether the gap is supportable or whether it reflects mismatched comparables, as it did in this case.

A Trim Mismatch, Corrected Through the Appraisal Process

This case is a clear example of how a single mismatched detail in an insurer’s comparable selection, trim level, can carry through an entire valuation if it isn’t caught and corrected. The vehicle owner’s total loss offer looked reasonable on paper until the comparables were checked line by line against the actual build of the vehicle.

If the insurance company’s total loss offer seems too low, Auto Praise can review the market valuation report and identify errors that may be affecting your settlement amount. We assist Florida vehicle owners statewide by reviewing comparable vehicles, adjustments, options, condition ratings, and valuation methodology to determine whether the offer is accurate.

A free claim review can help you understand whether there is a valid basis to challenge the insurance company’s valuation and pursue a better settlement.

Call 754-210-9807 for a Free Review Florida Licensed Adjusters • I-CAR Platinum Certified • IACP Certified Auto Appraisers