![]() Call us now:

Call us now:

Total Loss Appraisals

Independent Total Loss Appraisals to Challenge Insurance Valuations

Prepared by IACP Certified Auto Appraisers and Florida-Licensed Adjusters

IACP Certified Auto Appraiser

Florida Licensed Adjuster

20+ Years Insurance & Appraisal Experience

IACP Certified Auto Appraiser

Used by attorneys and vehicle owners statewide

Total loss valuation disputes are rarely about whether a vehicle qualifies as a total loss. They are about whether the insurer’s calculation of Actual Cash Value accurately reflects the real market. An undervalued ACV directly reduces the settlement amount paid to the vehicle owner.

Why Insurance Company Total Loss Offers Are Often Inaccurate

Use of CCC / Mitchell / Audatex without proper condition adjustments

• Incorrect comparable selection

• Missed options, trim, or regional market factors

• No physical inspection

• Internal pressure to settle quickly

What Clients Say

“Daryl took the time to explain the total loss process and reviewed the insurance valuation in detail.

The appraisal was thorough, professional, and clearly independent.”

— Verified Client Review

Independent appraisals prepared for insurance disputes, legal matters, and vehicle owners throughout Florida.

Our Easy Process & Free Claim Review

We review the insurance valuation and loss details for free

We analyze local market data and vehicle configuration

If you have a strong case, we prepare a defensible independent appraisal

We negotiate with the insurance appointed appraiser

- Our appraisals are prepared to withstand scrutiny from insurers, attorneys, and courts.

For a step-by-step overview of the entire claims process, you can review our Total Loss Claim Guide.

Need Help With a Total Loss Settlement?

If the insurance company’s total loss offer seems too low, Auto Praise can review the market valuation report and identify errors that may be affecting your settlement amount. We assist Florida vehicle owners statewide by reviewing comparable vehicles, adjustments, options, condition ratings, and valuation methodology to determine whether the offer is accurate.

A free claim review can help you understand whether there is a valid basis to challenge the insurance company’s valuation and pursue a better settlement.

Call 754-210-9807 for a Free Review

Florida Licensed Adjusters • I-Car Platinum Certified Auto Physical Damage Appraisers • IACP Certified Auto Appraisers

Understanding Total Loss Vehicle Criteria

In Florida, a vehicle is deemed a total loss when the cost of repairs reaches 80% its current market value. This determination can arise from accidents, theft, fire damage, flood damage, wind damage, hail damage, lightning strikes, or vandalism.

Key Factors

Insurance companies assess repair costs versus vehicle value to declare a total loss.

Who can use our service?

If you are filing a total loss claim against your own insurance, then you can invoke the appraisal clause in your policy to challenge the insurance company’s offer. This does not apply if you are fighting the offer from someone else’s insurance company that caused the damage to your vehicle.

Vehicle owners dealing with total loss claims in Florida may benefit from understanding the legal framework that governs these settlements. Our guide to Florida total loss law explains how these regulations affect the claims process.

Need an Independent Total Loss Appraisal?

If you believe your insurer undervalued your vehicle, an independent appraisal may be the next step.

Mastering the Art of Negotiating with Insurance Companies for Total Loss Claims

Navigating the insurance landscape during a total loss can be challenging. Our experts will negotiate for you with the insurance appointed appraiser, ensuring you receive the compensation you deserve.

Real Stories of Total Loss Success

Discover how we’ve helped clients navigate total loss appraisals. Our case studies highlight the significant impact of our expert evaluations.

Before: Insurance company valued the vehicle at $15,274

After: Actual cash value determined to be $18,953

Client saved $3,679 through our appraisal services

Florida Total Loss Appraisals: The Complete Guide to Understanding Your Options

What Is a Total Loss Appraisal?

A total loss appraisal is an independent certified valuation of your vehicle’s Actual Cash Value (ACV), the fair market value of your car immediately before it was damaged in an accident.

When an insurance company declares a vehicle a total loss, it means the cost to repair the vehicle is close to or exceeds the percentage of its value defined by law or company policy.

In Florida, that percentage is critical to understand because if your car’s repair costs exceed 80 percent of its pre loss value, it can legally be deemed a total loss under Florida Statute 319.30(3)(a).

Unlike insurance valuation systems that rely heavily on automated databases, our total loss appraisals involve manual review of comparables, factory options, and market specific adjustments to ensure accuracy.

At Auto Praise, we perform certified total loss appraisals that protect vehicle owners from undervaluation.

Our reports are USPAP compliant, supported by market data, and prepared by experts who understand collision damage, vehicle construction, and insurance valuation standards.

Before You Accept a Total Loss Offer

If the insurance valuation looks low, a quick review can identify common issues like incorrect comparables, missed options,

or improper condition adjustments.

Call to Speak With an Appraiser: 754-210-9807

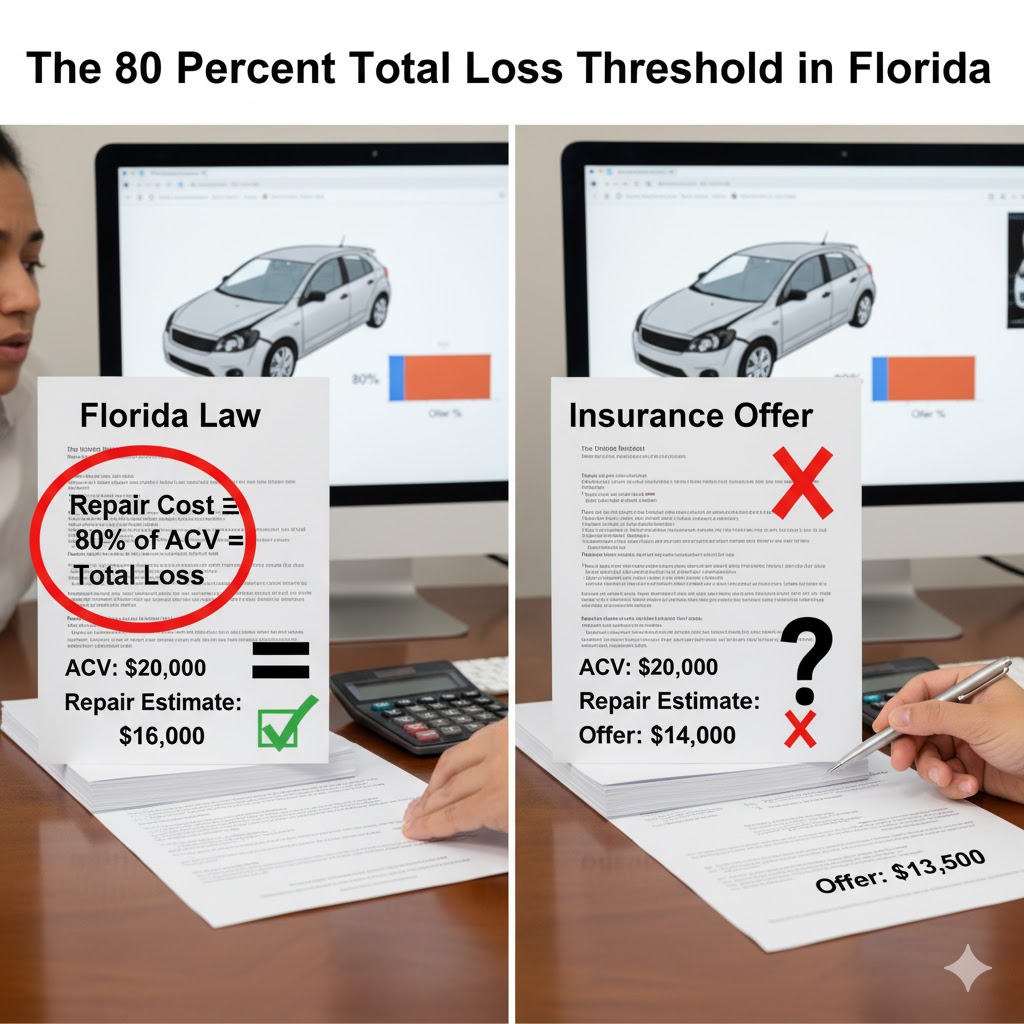

The 80 Percent Total Loss Threshold in Florida

Florida law defines a total loss when the cost to repair the vehicle equals or exceeds 80 percent of its Actual Cash Value before the loss.

Example:

If your vehicle was worth 30,000 dollars before the accident and the repair estimate is 24,000 dollars or higher, it is legally considered a total loss.

However, insurance companies often total vehicles before reaching that 80 percent mark.

Here is why.

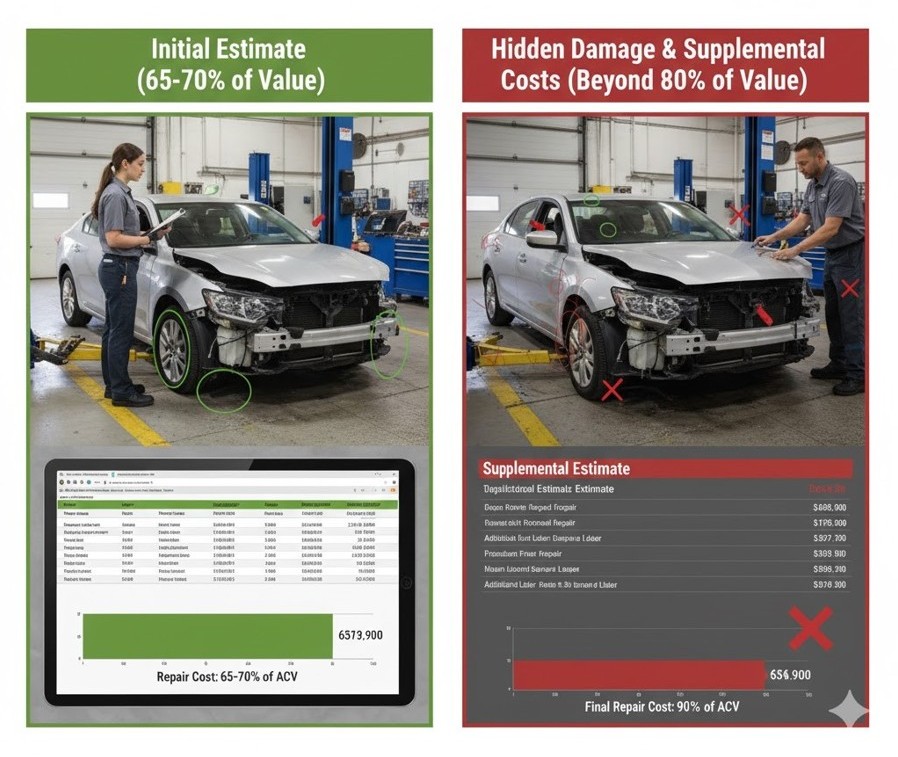

Why Insurance Companies Often Total Vehicles at 65 to 70 Percent of ACV

Insurance companies understand that repair estimates written at 65 to 70 percent of the vehicle’s value rarely reflect the true cost of repairs once work begins.

When a body shop disassembles the vehicle, additional hidden damage is almost always discovered, including structural issues, bent suspension components, or internal frame misalignment that was not visible during the initial inspection.

In addition:

Labor times and rates may increase depending on the shop’s location and workload.

Parts availability and pricing can change. Original equipment parts may be required if aftermarket components are not available or do not fit properly.

Supplemental estimates are almost always added once repairs begin.

These factors can easily push the repair costs beyond the 80 percent threshold, which is why insurers often choose to total vehicles once the estimate approaches 65 to 70 percent.

How Insurance Valuation Systems Determine ACV

Most insurance carriers rely on third-party valuation vendors to generate market reports. These systems identify comparable vehicles, apply algorithm-based mileage and condition adjustments, and produce a settlement figure.

However, these systems depend entirely on correct inputs. Incorrect trim decoding, missing options, mismatched comparables, or improper geographic selection can significantly affect the final number.

A total loss appraisal involves verifying those inputs rather than accepting automated outputs at face value.

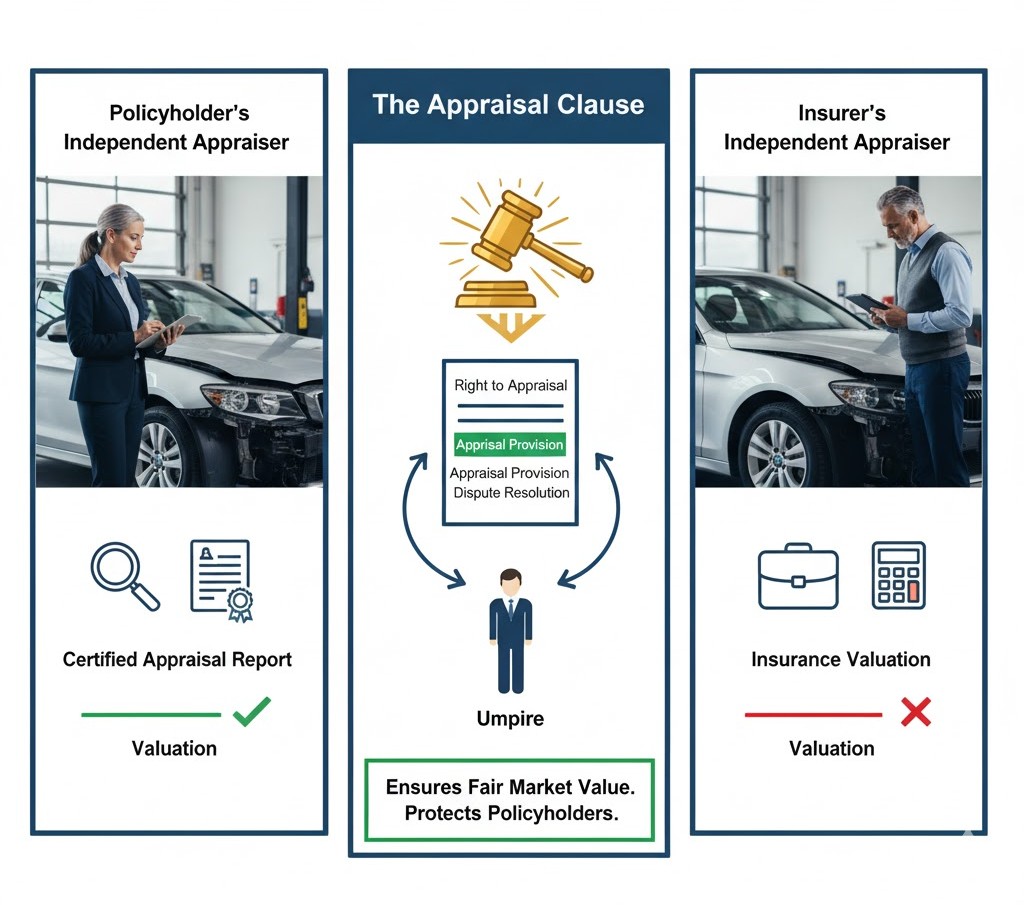

Understanding the Appraisal Clause

The appraisal clause is a standard provision found in most auto insurance policies that allows either the insurer or the policyholder to dispute the value of a total loss settlement.

This clause gives both parties the right to hire independent appraisers to determine the vehicle’s fair market value when there is a disagreement.

You will typically find this section under headings such as:

Right to Appraisal,

Appraisal Provision, or

Dispute Resolution.

It ensures that vehicle owners are not forced to accept an insurer’s valuation without the opportunity for an independent review.

Step-by-Step Guide

If this is a first-party claim (your own policy), this guide explains how the appraisal clause works and how to invoke it correctly.

Read: Invoking the Total Loss Appraisal Clause

Read: Invoking the Total Loss Appraisal Clause

Who Can Invoke the Appraisal Clause

Only first party insureds, meaning those filing a claim under their own insurance policy, can invoke the appraisal clause.

If you are filing a third party claim against another driver’s insurance company, you do not have an appraisal clause available because you are not a party to their contract.

However, you can still challenge their offer through an independent total loss appraisal prepared by Auto Praise, which serves as documented evidence of the vehicle’s true pre loss market value, though they are not bound to honor it.

How the Total Loss Process Works

- Contact a Certified Appraiser for a Claim Review

Before invoking the appraisal clause, contact Auto Praise for a claim review.We analyze the insurer’s valuation report, review market comparables, and determine whether the settlement offer appears fair.If it is undervalued, we will advise you on the next steps.

- Notify the Insurance Company

Once you decide to move forward, you must formally invoke the appraisal clause in writing. This notice communicates that you disagree with the insurer’s valuation and wish to begin the independent appraisal process.

- Each Side Hires Their Own Appraiser

You hire your independent appraiser.The insurance company hires its own appraiser to represent its interests.Both appraisers must remain impartial, even though each was selected by one side.

- Negotiation Between Appraisers

Both appraisers review vehicle data, comparable listings, condition reports, and valuation sources such as J D Power, Black Book, or Carfax listings. They then attempt to reach an agreement on the Actual Cash Value of your vehicle.

- If They Cannot Agree, an Umpire Is Involved

If the two appraisers cannot agree, they jointly select a neutral third party known as an umpire. The umpire reviews both appraiser’s findings and decides which valuation is most accurate.

- The Final Decision

When any two of the three parties, either both appraisers or one appraiser and the umpire, agree on the value, that number becomes legally binding under the policy.

Key Factors That Affect Vehicle Value

When performing a total loss appraisal, several elements can significantly influence your vehicle’s market value:

Prior Accidents or Claims

- Aftermarket Modifications

- Vehicle History Reports

- OEM Options and Upgrades

- Regional Market Trends

Market Volatility and Timing of Loss

Used vehicle markets fluctuate based on supply constraints, seasonal demand, and regional inventory levels. A defensible total loss valuation must reflect the market as it existed on the date of loss.

During periods of elevated pricing, outdated comparable data may understate value. Proper analysis considers current market conditions rather than relying solely on historical data.

Tips for Negotiating With the Insurance Company

If you are a third party claimant dealing with the at fault driver’s insurer, then the insurance carrier is not bound by the appraisal clause, but you still have negotiation power. Here is how to strengthen your position:

- Request a detailed valuation report showing how the insurer determined your car’s value, including the comparable vehicles used.

- Review the comps carefully. Insurers sometimes use vehicles that are not truly comparable, such as different engine and transmission configurations, trims or missing options.

- Provide your own supporting evidence such as local listings of similar vehicles in comparable condition.

- Stay professional and factual throughout the negotiation. Focus on data, documentation, and fairness.

Common Issues That Lead to Undervalued Total Losses

One of the most frequent issues in total loss valuation is the misidentification or omission of factory options, particularly on higher end vehicles where equipment packages can significantly change the market value.

Insurance companies often rely on automated VIN decoding systems that may not capture factory installed upgrades such as:

- Adaptive cruise control

- Premium sound systems

Advanced safety technology

Performance or appearance packages

These features can alter a vehicle’s market value by thousands of dollars, yet they are often missed in insurance valuations.

At Auto Praise, when valuing high end luxury vehicles, we manually verify every factory option using the manufacturer’s build data to ensure that your pre loss valuation is complete and accurate.

When an Independent Total Loss Appraisal Is Most Effective

- Higher trim or premium vehicles with complex option packages

- Recently purchased vehicles with strong market demand

- Vehicles in above-average condition

- Settlement offers that appear significantly below local listing prices

- Cases where VIN decoding errors are identified

In these situations, documented market evidence can materially change the settlement outcome.

Get a Professional Total Loss Appraisal in Florida

If your vehicle has been declared a total loss and you believe the insurer’s offer is too low, you have the right to challenge their valuation.

A certified total loss appraisal from Auto Praise can make the difference between settling for less and receiving the fair value you deserve.

If your vehicle was repaired instead of declared a total loss, you may be dealing with diminished value rather than an Actual Cash Value dispute. In those cases, a diminished value appraisal may be appropriate.

Request a Professional Total Loss Claim Review

Before accepting a total loss settlement, have the valuation reviewed for configuration accuracy, comparable selection, and market alignment. A certified independent appraisal provides objective evidence that can support negotiations or formal appraisal proceedings.

Call 754-210-9807 to speak directly with a certified appraiser and determine whether your settlement reflects true market value.

Understanding the Costs and Practical Considerations of Appraisal

The appraisal clause process requires each side to hire its own appraiser. If the appraisers cannot agree, a neutral umpire is selected, and both parties typically share the umpire’s fee.

While appraisal can correct undervaluations, it is important to weigh the potential settlement difference against the cost of the process. A claim review helps determine whether invoking appraisal is strategically appropriate.

Understanding Total Loss Claims: Related Guides

Total loss claims involve several factors including Florida insurance law, valuation methods, comparable vehicles, and settlement negotiations. The following guides explain how total loss claims are handled and what options vehicle owners may have when disputing an insurance settlement.

- Florida’s Total Loss Law Explained: Understanding the 80% Rule

- How to Challenge Your Insurance Company’s Total Loss Offer

- Step by Step Guide: Invoking the Total Loss Appraisal Clause

- What Happens When Your Car Is Declared a Total Loss in Florida

- How Insurance Companies Determine the Value of a Total Loss Vehicle

- What To Do If Your Insurance Company Undervalued Your Car in a Total Loss

- Comparable Vehicles in Total Loss Valuation

- Can You Keep Your Car After a Total Loss in Florida?

- Total Loss Settlement Negotiation

Frequently Asked Questions – Florida Total Loss Appraisals

What is the total loss threshold in Florida?

In Florida, a vehicle is generally considered a total loss when the cost to repair it plus its salvage value equals or exceeds 80% of the vehicle’s actual cash value (ACV). This is commonly referred to as Florida’s total loss threshold. However, insurers may still declare a vehicle a total loss below this percentage depending on safety concerns, parts availability, or internal valuation practices. An independent total loss appraisal evaluates whether the ACV was calculated correctly, not whether the insurer chose to total the vehicle.

Who can invoke the appraisal clause in a Florida total loss claim?

In Florida, the appraisal clause typically applies to first-party claims filed under your own insurance policy. Either the policyholder or the insurance company may invoke the appraisal clause when there is a dispute over the vehicle’s value. Third-party claims, which are handled through the at-fault driver’s insurance, generally do not include appraisal clause rights unless the insurer voluntarily agrees to participate.

What is the difference between a first-party and third-party total loss claim?

A first-party total loss claim is filed under your own insurance policy and is governed by the terms of that policy, including any appraisal clause. A third-party total loss claim is filed against another driver’s insurance company and is handled under liability rules, not your policy. The available dispute options and valuation leverage can differ significantly depending on which type of claim applies.

Can I dispute a total loss value after the insurance company makes an offer?

Yes. Receiving a settlement offer does not require you to accept it. Florida vehicle owners commonly dispute total loss valuations when incorrect comparables are used, vehicle options are missed, condition adjustments are inaccurate, or local market data is ignored. An independent total loss appraisal helps determine whether the insurer’s valuation reflects the vehicle’s actual pre-loss value.

What does an independent total loss appraisal do?

An independent total loss appraisal provides an unbiased opinion of the vehicle’s actual cash value as of the date of loss. The appraisal is prepared independently of the insurance company and may be used during settlement negotiations, appraisal clause proceedings, or legal disputes. While it does not guarantee a specific outcome, it provides documented valuation support that can be relied upon during the dispute process.

Get Your Free Consultation Today

Phone

Help & Support: support@auto-praise.com

Inquires: info@auto-praise.com

Your Voices are Our Upgrades! Revamped Elementor Testimonials

Experience the power of authentic testimonials with refreshed styles, responsive designs, and advanced display options. Let your customer voices shine and captivate your WP website visitors effortlessly.

This option is available in Premium Addons Pro.

This option is available in Premium Addons Pro.

This option is available in Premium Addons Pro.

Premium Addons’ Customer Reviews on WordPress.org